- Julian Seethaler

- 10.07.26

- 2 min

- For SME, EIC Accelerator, EU funding programmes,

With an amendment to its 2026 work programme, the European Innovation Council (EIC) is, for the first time, allowing defence and dual-use ...

You've previously learned why it's worth preparing a sustainability report in our 10 good reasons for sustainability reporting blog article. The following article introduces the CSRD and explains the consequences of the new guideline for sustainability reporting.

Please note the current developments under the EU Omnibus Initiative (as of 25 February 2025), which suggest potential easing of sustainability requirements, including the CSRD. You can find all key information about the envisaged changes in our blog post.

CSRD stands for Corporate Sustainability Reporting Directive. It is an extension of the Non-Financial Reporting Directive (NFRD). With the CSRD as a cornerstone of the European Green Deal, the topic of sustainability reporting is now to be raised to the same level as financial reporting.

With the Non-Financial Reporting Directive (NFRD), large companies have already been legally required to disclose non-financial aspects of their corporate activities since 2014 (EU law) and 2017 (German law). In November 2022, the EU adopted the Corporate Sustainability Reporting Directive (CSRD). It extends both the content to be reported and the group of companies subject to reporting requirements. As a result, listed small and medium-sized enterprises (LSMEs) as well as small and non-complex credit institutions and captive insures will also be subjected to a reporting obligation, starting in business year 2026.

All content must refer to the 1.5-degree target. A mandatory external review of the reports has also been added.

The CSRD also expands the group of companies subject to reporting requirements. The reporting obligation for the CSRD takes effect in multiple stages.

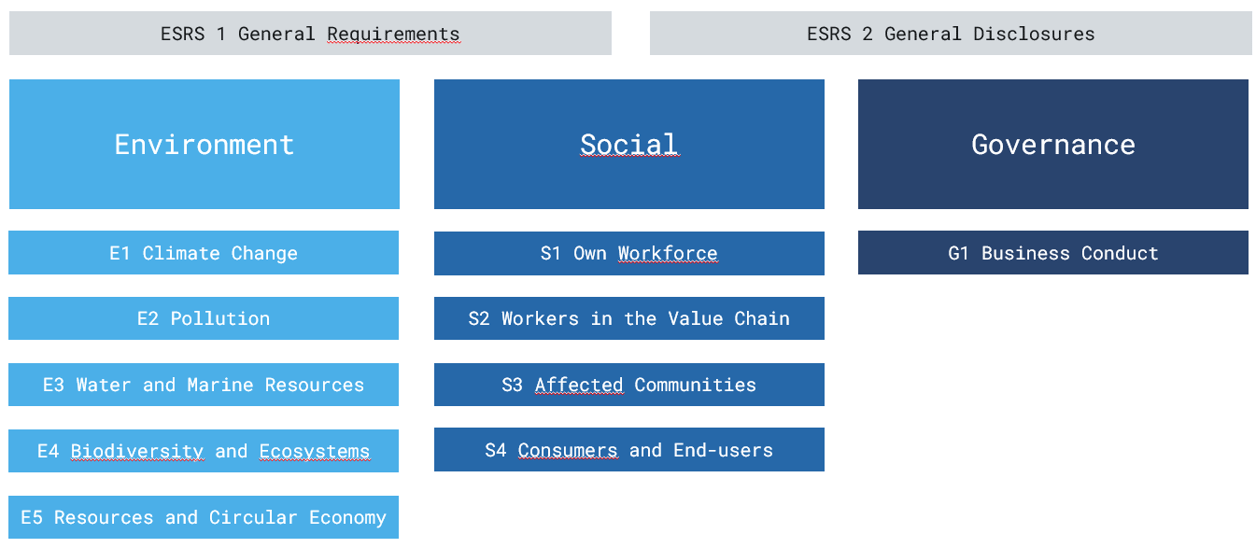

Based on the CSRD, European reporting standards were adopted in 2023, which provide companies with an uniform framework for reporting within the EU and contribute to the comparability of the reports: ESRS (European Sustainability Reporting Standards). In addition to the sector-agnostic standards, which shall be applied starting from 01/01/ 2024, EGRAG (European Financial Reporting Advisory Group) is currently working on the development of the sector-specific standards. Furthermore, the first drafts of the uniform standards for listed SMEs (LSME, listed small- and medium-sized enterprises) and non-listed and therefore voluntarily reporting SMEs (VSME, voluntary small- and medium-sized enterprises) were published on 22 January 2024. These provide for simplifications and reductions in reporting obligations. The consultation on these drafts is open until May 21, 2024.

Supporting standards, such as the German Sustainability Code (DNK) or the SDGs of the United Nations, can be helpful for training purposes and for the first introduction to sustainability reporting. Some of your clients may also require specific disclosures that can be verified using other standards or ratings, e.g. GRI, CDP, SBTi, EcoVadis, etc. However, these cannot replace the ESRS for undertakings which are subject to reporting requirements and must be implemented parallel to the European standards accordingly to the specific customer request.

Text: Katharina Prontnicki, Olga Schmidt

EurA AG

T- 079619256-0Max-Eyth-Straße 2

73479 Ellwangen

info@eura-ag.com